Understanding Florida Property Taxes and Insurance

If you are shopping for a Home Equity Line of Credit (HELOC) in Florida, you’ve probably spent some time playing around with online financial tools. You type in your estimated home value, your current mortgage balance, click a button, and watch a clean monthly payment estimate pop up on your screen.

National platforms love to use automated estimation templates to guess your holding costs. However, Florida does not fit into a standard automated box. Our state features highly localized property tax structures and an incredibly unique property insurance landscape.

When a lender calculates your debt-to-income (DTI) ratio to approve your new equity line, your actual tax and insurance bills play a massive role. At FloridaHELOCLine.com, we throw out generic forecasting algorithms in favor of absolute real-world data.

Here is exactly how your local property taxes and insurance impact your HELOC qualification—and why manual accuracy is the key to maximizing your approval.

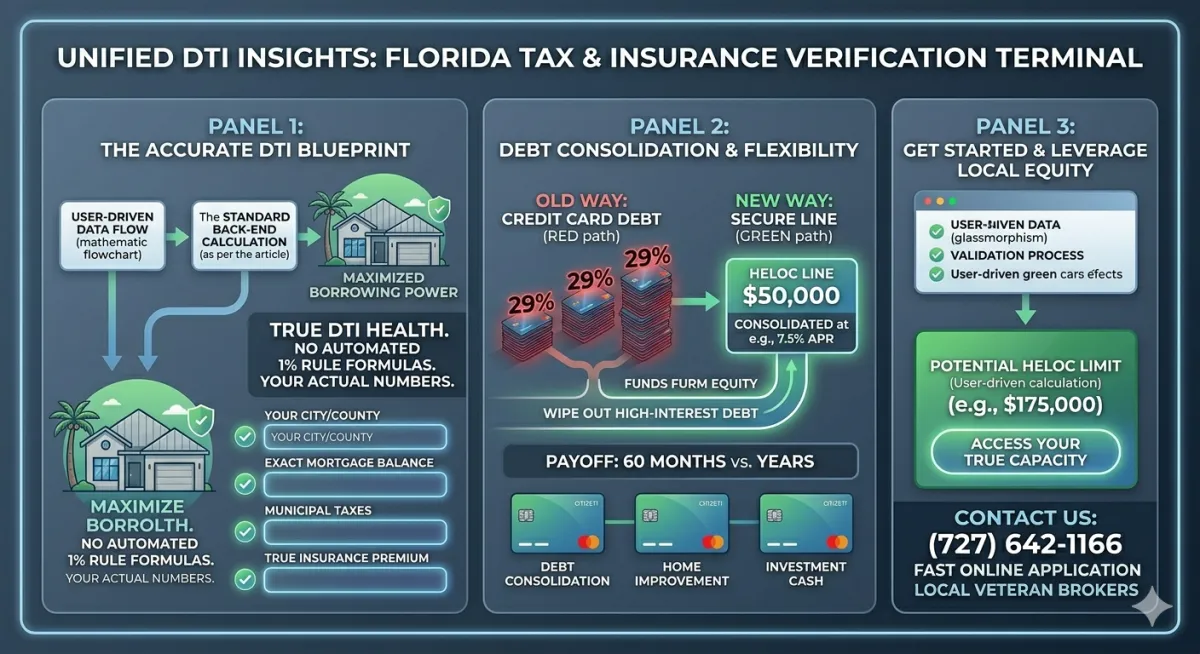

### 1. The DTI Equation: Where Taxes and Insurance Hinder or Help

To approve your HELOC, a underwriter looks closely at your Debt-to-Income (DTI) ratio. This is the percentage of your gross monthly income that goes toward paying your recurring monthly debts.

Lenders divide this into two parts, but for a second mortgage, your Back-End DTI is what matters most. This includes:

Primary Mortgage (P\&I) + Property Taxes + Homeowners Insurance + HOA Fees + Other Fixed Debts + Proposed HELOC Payment

Because your property taxes and insurance premiums are legally tied to the house, they are permanent components of your housing debt. If an automated algorithm overestimates these figures, your DTI looks artificially inflated, which can lead to a lower credit limit approval or an outright denial. Conversely, if an algorithm underestimates them, you run the risk of budgeting for a payment you can't actually afford.

### 2. The Florida Property Tax Variable: Why Location Controls the Math

You cannot calculate a Florida HELOC payment using a flat state average. Property tax assessments in Florida are strictly localized and highly regulated under the state's Save Our Homes (SOH) act.

The Save Our Homes Cap: This amendment caps increases in the assessed value of a primary homesteaded property at 3% per year, or the percent change in the Consumer Price Index (CPI), whichever is lower.

The Reassessment Trap: If you purchased your Florida home recently, your property tax bill is likely vastly different from a neighbor who has lived in an identical house for fifteen years. When a property transfers ownership, the assessment resets to full market value.

Because of this, an automated tool guessing your tax liability based on basic zip code data will often wildly miss the mark. To protect your borrowing power, your file requires a manual look at your actual current county trim notice.

### 3. The Florida Insurance Landscape: Factoring in True Costs

It is no secret that property insurance in the Sunshine State has undergone major shifts. While structural state reforms have introduced welcomed stability and invited new private carriers back into the market, premiums still vary significantly based on geography, home age, and structural wind mitigation features.

When qualifying for a HELOC:

Wind Mitigation Matters: A home in the Tampa Bay area or Miami with modern hurricane straps, a new roof, and impact windows will carry a fraction of the insurance premium compared to an un-renovated property of the same size.

Flood Insurance Mandates: Depending on your specific flood zone designation, a lender may require a separate flood policy. This adds another fixed monthly line item to your DTI calculation.

A generic calculator using standard assumptions completely misses these critical details.

### Take Control of Your Home Equity

Securing a HELOC is a brilliant tactical move to consolidate high-interest credit cards, fund necessary home renovations, or access liquid investment capital. But don't let a generic internet tool compromise your approval capacity before you even speak to a professional.