How Much Equity Can I Withdraw From My Florida Home?

If you are watching Florida property values remain resilient in 2026, you are likely wondering exactly how much of that built-up wealth you can convert into usable cash. Whether you want to fund a major home renovation, invest in another property, or clear out high-interest debt, your home is your strongest financial tool.

But how do lenders determine your final credit limit?

At FloridaHELOCLine.com, we cut through the confusion. We don't use automated, generic percentage rules that guess your local holding costs. Instead, we use your actual data to show you the precise math behind your maximum borrowing power.

Here is exactly how to calculate your maximum equity withdrawal in Florida today.

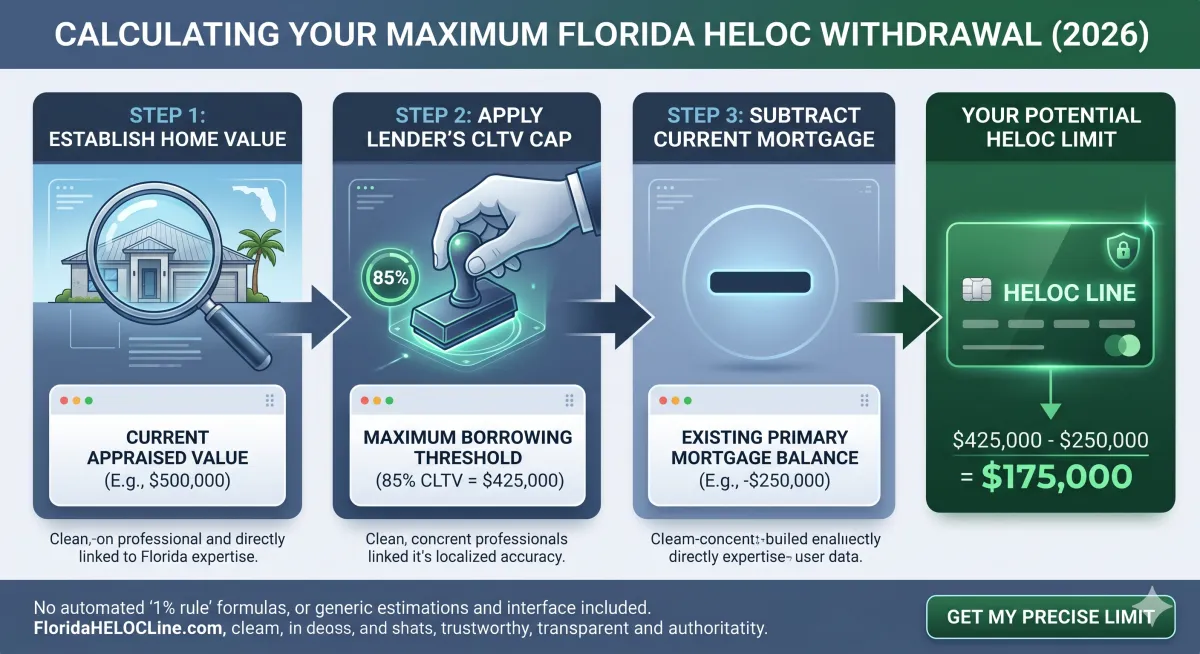

### The Key Formula: Understanding CLTV

When you apply for a Home Equity Line of Credit (HELOC), lenders don't just look at your equity; they look at your Combined Loan-to-Value (CLTV) ratio. This ratio combines your existing primary mortgage balance with the new credit line you want to open, comparing the total against your home's current appraised value.

In the 2026 lending landscape, standard guidelines typically cap your maximum CLTV between 80% and 85% of your home's total value. However, if you have an elite credit profile and strong, verifiable income, select specialized programs can push your borrowing capacity up to 90% or even 95% CLTV.

### Step-by-Step: Calculate Your Real Limit

To find your number, you only need to complete three simple calculations:

Step 1: Determine Your Current Home Value

Forget outdated estimates from generic websites. Look at recent, hyper-local comparable sales in your specific Florida neighborhood to establish a realistic baseline.

Example: Let's say your home is currently worth $500,000.

Step 2: Apply the Lender's Maximum CLTV Cap

Multiply your home’s value by a standard conservative lending limit (like 85%) to establish your absolute maximum allowed borrowing threshold.

Math: $500,000 \times 0.85 = $425,000 total borrowing capacity.

Step 3: Subtract Your Existing Mortgage Balance

Take that borrowing capacity and subtract exactly what you currently owe on your primary mortgage.

Math: If you owe $250,000 on your first mortgage:

$425,000 - $250,000 = $175,000

Your Maximum Potential HELOC Limit: $175,000.

### Why Local Context Changes the Math

Many national, automated lending platforms will generate generic numbers that completely fall apart when applied to Florida. They fail to factor in our state's unique local variables, such as:

Florida Documentary Stamp Taxes: State taxes levied directly on discretionary notes and second mortgages.

Hyper-Local Insurance & Taxes: Because property taxes and homeowners insurance vary wildly from county to county across Florida, a rigid internet calculator cannot give you an accurate debt-to-income (DTI) projection.

That is why our platform at FloridaHELOCLine.com relies entirely on manual user inputs. You provide your exact real-world expenses, and we build a highly customized, structurally sound financing option based on your 23-year broker network.

### Ready to Unlock Your Accurate Numbers?

Don't guess your financial future with automated algorithms. Use a platform designed specifically for Florida homeowners. Come to the site, input your real figures, and get an immediate, accurate assessment of your borrowing power.