How Fed Rate Decisions Affect Your Florida HELOC Payment

When you turn on the news, the talking heads are constantly obsessing over the Federal Reserve. They break down every word from the Federal Open Market Committee (FOMC) like it's a state secret.

But if you are a homeowner, you only care about one thing: How do these massive macroeconomic moves affect the money leaving my bank account every month?

If you have a Home Equity Line of Credit (HELOC) or are planning to open one at FloridaHELOCLine.com, understanding the direct pipeline between the Federal Reserve and your checkbook is critical.

Unlike fixed-rate first mortgages, HELOCs have a front-row seat to Fed policy. Here is exactly how it works.

### The Direct Pipeline: Fed Funds Rate affects Your HELOC rate.

To understand your payment, you have to look at the chain reaction that happens every time the Fed makes a move.

The Fed Funds Rate: This is the baseline interest rate banks charge each other for overnight loans.

The U.S. Prime Rate: This is the benchmark rate commercial banks charge their most creditworthy corporate customers. By industry standard, the Prime Rate is pegged exactly 3.00% higher than the upper bound of the Fed Funds Target Range.

Your HELOC Margin: When you secure a line of credit through a local broker, your rate is structured as a simple equation: Prime Rate + Your Margin (your margin is a fixed percentage based on your credit score, CLTV, and financial profile).

Because a HELOC is a variable-rate product, its base rate shifts in lockstep with the Prime Rate. When the Federal Reserve adjusts its baseline target, your variable rate typically adjusts within one to two billing cycles.

### The 2026 Rate Landscape: A Lesson in Stability

After a period of policy easing that brought the Fed's target down to the 3.50%–3.75% range (pinning the U.S. Prime Rate firmly at 6.75%), the Federal Reserve has taken a cautious, stable approach through mid-2026. The central bank has held baseline borrowing costs steady to monitor broader inflationary pressures, particularly around energy and supply chains.

For Florida homeowners utilizing a line of credit, this current landscape offers a highly predictable environment. Instead of the wild, sudden payment spikes seen during previous tightening cycles, today's variable-rate borrowers are experiencing stable, range-bound monthly interest costs.

### The Math: How a 0.25% Shift Alters Your Payment

When the Fed does move, how much does your payment actually change? Let's look at the raw numbers.

Most HELOCs feature an "Interest-Only" draw period for the first 10 years, meaning your monthly payment is calculated strictly on your outstanding balance and current rate.

Let's assume you have an outstanding balance of $50,000 on your line of credit:

At a 7.00% HELOC Rate (Prime + Margin):

$50,000 x 0.07/12 = $291.66 per month

If the Fed cuts rates by 25 basis points (0.25%), dropping your rate to 6.75%:

$50,000 x 0.0675/12 = $281.25 per month

Your Direct Savings: $10.41 per month for every $50,000 borrowed.

While a single 25-basis-point drop sounds minor, a series of cumulative cuts over time can result in hundreds of dollars back in your annual household budget.

### Why Local, Manual Calculations Trim the Fat

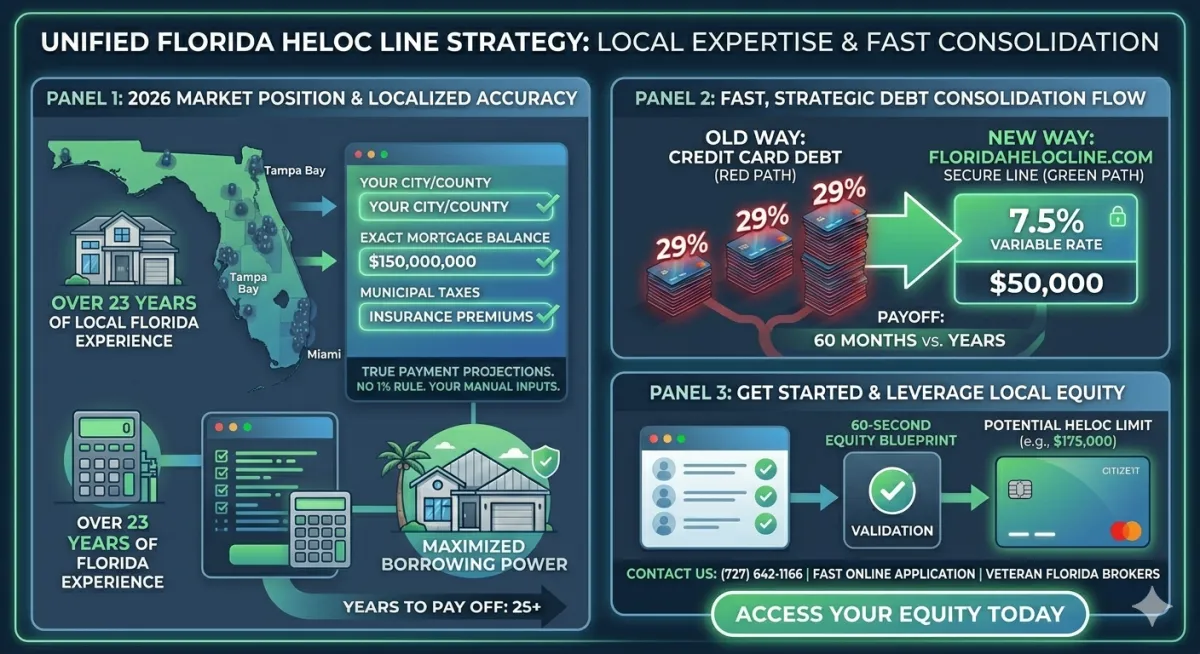

National automated lending platforms love to use standard, rigid software code to estimate what a homeowner's macro budget looks like. They take a wild guess at your holding costs, frequently applying automated percentage formulas that inflate your projected debt ratios and limit your true borrowing capacity.

We throw that outdated approach in the trash. At FloridaHELOCLine.com, we know that a homeowner in Tampa faces an entirely different property tax and insurance environment than someone in Jacksonville.

Our custom portal bypasses automated algorithms completely, allowing you to manually input your exact home expenses. This level of localized precision gives us an airtight view of your true debt-to-income (DTI) health, enabling us to maximize your equity line approval regardless of where the Federal Reserve sets its benchmarks.

### Take Control of Your Financial Leverage

You cannot control what the Federal Reserve decides at its next meeting, but you can control how you leverage your wealth. In a stabilized rate environment, securing a flexible line of credit is an elite tool to wipe out stagnant debt, protect your low first mortgage, or deploy liquid capital into new investments.

Get Your Accurate, No-Obligation Equity Blueprint

Skip the algorithmic guesswork. Put your real-world numbers into our manual calculator to map out a precise, optimized equity line tailored to your home.