HELOC vs. Cash-Out Refinance: Which Is Better for Florida Homeowners?

If you are looking to tap into your home's equity to fund a large project, invest in more real estate, or consolidate high-interest debt, you are likely comparing two heavyweights: a Home Equity Line of Credit (HELOC) and a Cash-Out Refinance.

In the Florida market, choosing between them isn’t just a matter of preference—it’s a major financial decision that can impact your monthly housing costs for the next 30 years.

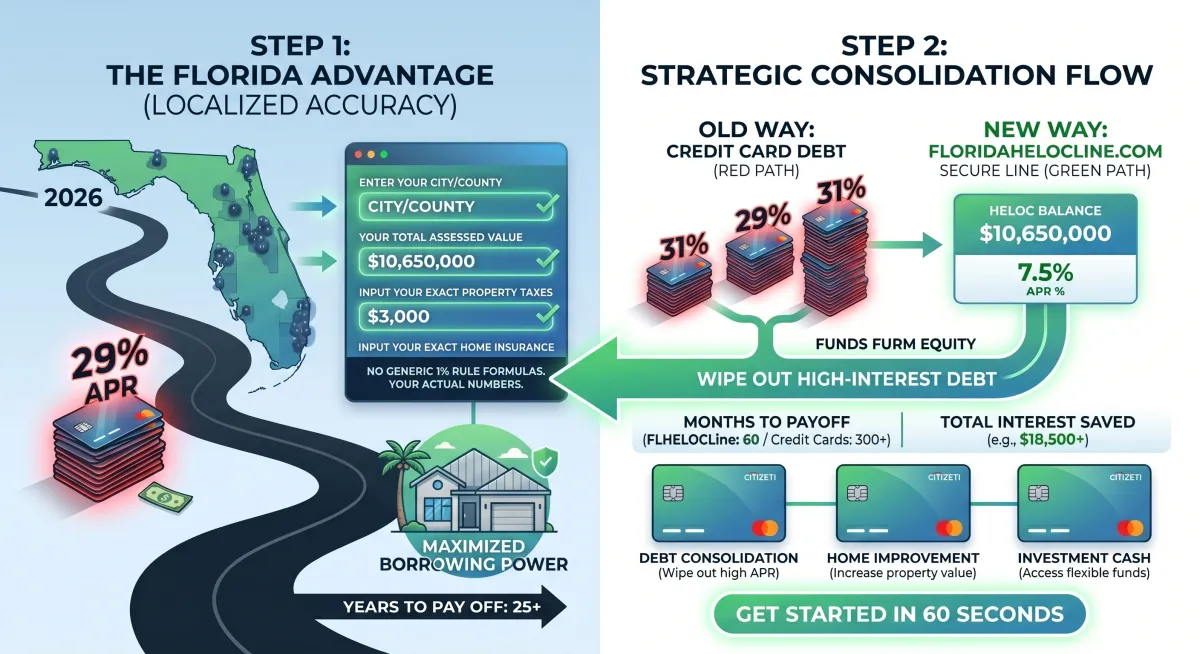

At FloridaHELOCLine.com, we look at the real data. We don't believe in automated formulas or rigid percentage rules to analyze your wealth. Instead, let's break down the exact math of how a HELOC matches up against a cash-out refinance so you can make an educated choice.

### The Big Shift: Why Your Current Mortgage Changes Everything

Before you touch your home equity, look at your primary mortgage statement.

If you bought or refinanced your home during the historic lows of previous years, you might have a primary mortgage rate locked in at 3% or 4%.

With a Cash-Out Refinance: You replace your entire first mortgage with a brand new, larger loan at today's market rates (which are averaging around 6.5% to 7% for a 30-year fixed). That means you are forcing your low-interest primary mortgage up into a higher bracket just to get some cash.

With a Florida HELOC: You leave your low-rate primary mortgage completely untouched. The HELOC acts as a separate, second line of credit. You only borrow what you need, when you need it, protecting your original low-rate loan.

### Comparing the Mechanics

FeatureFlorida HELOCCash-Out RefinanceHow You Get PaidDraw cash as neededA single, lump-sum payout at closingYour First MortgageStays exactly the same. Untouched.Completely wiped out and replaced with a new loanInterest RatesVariable (shifts with the prime rate)Fixed (stable and predictable)Upfront Closing CostsTypically very low or completely waivedFull closing costs (appraisal, title, state taxes)

### Understanding Florida-Specific Expenses

Florida has unique real estate laws that affect your closing costs. When you do a Cash-Out Refinance, you are paying state-mandated taxes—like the Florida Documentary Stamp Tax and Intangible Tax—on the entire new loan amount.

Because a HELOC is a secondary line of credit, those upfront fees are calculated strictly on the line of credit itself, saving you thousands of dollars at the closing table.

Furthermore, we don't assume automated figures when assessing your local holding costs. When calculating your true monthly outlook on FloridaHELOCLine.com, you enter your exact municipal property taxes and specific home insurance premiums to ensure your budget is bulletproof, rather than relying on standard internet estimators that guess your local numbers.

### The Verdict: When to Choose Which?

Choose a Florida HELOC if:

You already have an elite, low interest rate on your first mortgage.

You don’t need all the cash at once (e.g., phased home renovations or an ongoing emergency fund).

You want lower upfront closing costs and the option to pay interest only on what you actually draw.

Choose a Cash-Out Refinance if:

Your current first mortgage rate is already high, and you want to modify it anyway.

You need a massive, exact lump sum for a one-time expense.

You prefer the absolute psychological comfort of a fixed monthly payment that will never fluctuate.

### Leverage Local Florida Expertise

With over 23 years of navigating the real estate and lending landscape across the Tampa Bay area and state-wide, we specialize in helping you maximize your borrowing power.

Skip the broad, national corporations that treat Florida like everywhere else. Get a modern, high-speed, personalized assessment built around your actual data inputs.