2026 Florida Real Estate Outlook: Is It the Right Time to Tap Your Equity?

For the past several years, the Florida real estate market felt like a runaway train. Prices skyrocketed, inventory completely vanished, and panic-buying became the norm.

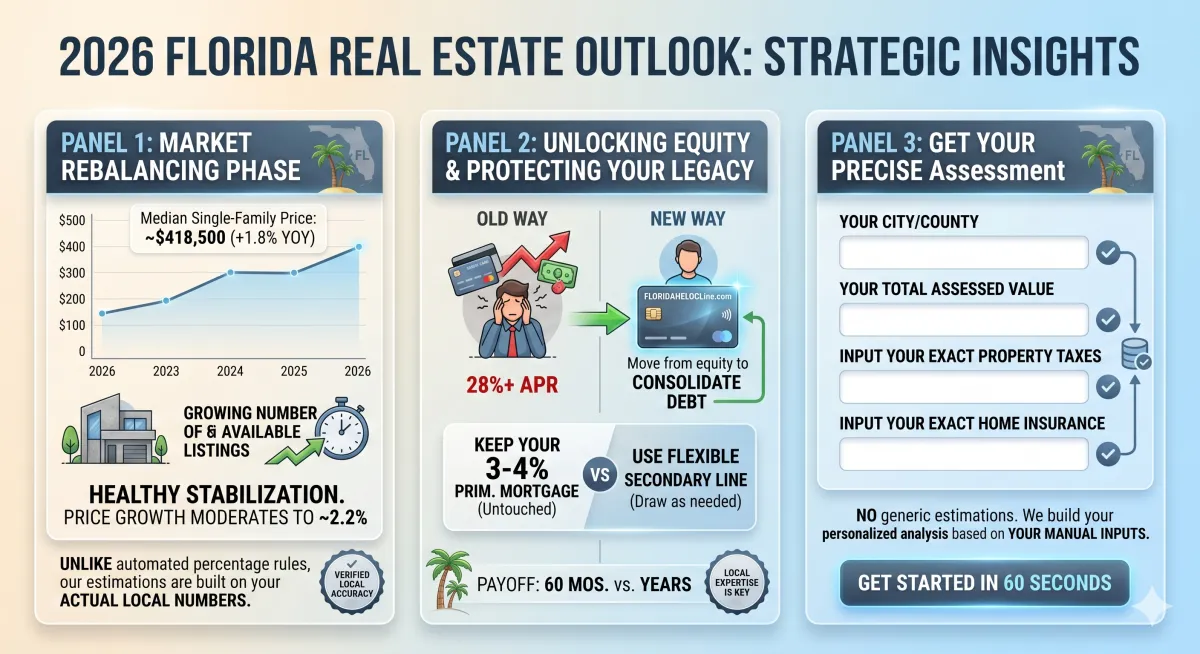

Now that we are moving through mid-2026, the narrative has fundamentally changed. The market is firmly locked into a "healthy rebalancing" phase. Prices are stabilizing, housing inventory has trended back toward healthier levels, and buyers finally have room to breathe.

If you own property in the Sunshine State, this shift brings up a massive financial question: With the market normalizing, is 2026 the right time to pull equity out of your home, or should you wait?

At FloridaHELOCLine.com, we look at real-time local dynamics—not rigid national models or automated percentage rules—to guide your decisions. Here is the ground truth on the 2026 Florida landscape.

### Ground Check: Where Do Florida Home Values Stand Today?

Despite rumors of a market crash, the actual data tells a story of stabilization.

Across the state, the median single-family home price has settled in the $417,000 to $420,000 range, holding strong at roughly a 1.8% year-over-year increase. In highly demanded hubs like the Tampa Bay area, median single-family home prices have stubbornly plateaued around $400,000 for the last two years running.

What this means for your equity: Your home equity is secure. Even though the double-digit appreciation jumps of the post-pandemic boom are behind us, the equity you built over the last few years isn't evaporating. It is sitting firmly in your property, waiting to be leveraged.

### Why Mid-2026 is a Prime Window for a HELOC

Waiting for home values to skyrocket further is a flawed strategy for the remainder of this year. Experts project a modest 2.2% growth path for statewide home prices through late 2026.

Because values are holding a steady baseline, this is an incredibly strategic window to establish a Home Equity Line of Credit (HELOC) for three key reasons:

1. 30-Year Fixed Rates Are Range-Bound

Standard 30-year fixed mortgage rates have largely leveled out, expected to float between 6.0% and 6.4% for the rest of the year. If you are one of the millions of Floridians holding a primary mortgage rate down at 3% or 4%, a Cash-Out Refinance makes zero sense right now because it forces you to reset your entire loan to a higher bracket. A HELOC lets you keep your primary low rate untouched.

2. Escape Rising Consumer Debt Costs

While home prices are tracking at a normal, stable rhythm, the cost of unsecured debt has gone through the roof. Credit cards and personal loans are hitting historic peaks. Tapping your home equity at a significantly lower variable rate to wipe out toxic high-interest balances is the fastest way to save hundreds of dollars in monthly cash flow this year.

3. Fund Highly Insulated Home Upgrades

As inventory grows across Florida (active listings rose significantly to roughly a 4.7-to-5 month supply), properties are staying on the market a bit longer. Buyers are demanding homes in absolute move-in condition. Using a HELOC to upgrade your roof, renovate a kitchen, or install impact windows ensures your property remains elite and highly competitive if you decide to sell down the road.

### Avoid the "Generic Calculator" Trap

The biggest mistake a Florida homeowner can make in 2026 is using a generic national algorithm to map out their borrowing limits.

Florida’s holding costs are entirely unique. While we are seeing a welcomed stabilization in home insurance thanks to new private carriers entering the state market, premiums and local property taxes vary wildly from Jacksonville down to Miami.

That is why FloridaHELOCLine.com completely throws out automated estimation rules. Our custom platform is powered strictly by your manual entries. You provide your exact mortgage balance, your specific county tax bill, and your actual insurance premium. This allows us to construct a mathematically precise debt-to-income projection that actually protects your financial health.

### The Bottom Line

Is it the right time? Yes. The 2026 market has shifted from a chaotic gamble into a highly predictable, rational environment. Your equity has peaked and stabilized; borrowing conditions are steady, and consumer interest rates are too high to ignore.

Don't leave your wealth locked behind a front door. Turn your real estate success into active financial leverage.