2026 Equity Playbook: HELOC Trends vs. Cash-Out Refinance in Florida

As we move through mid-2026, the math behind unlocking home equity has completely changed. For years, soaring home values made any equity withdrawal look like an easy win. But today’s stabilizing real estate market and unique interest rate landscape require a much more tactical approach.

If you are looking to tap your property’s wealth for debt consolidation, home improvements, or investment capital, you are likely looking at two main pathways: a Home Equity Line of Credit (HELOC) or a Cash-Out Refinance.

At FloridaHELOCLine.com, we cut through national generalities. We don't rely on rigid, automated software formulas that guess your holding costs. Instead, let's break down how 2026 market trends and shifts in Florida property values are directly dictating your borrowing power.

### The 2026 Trend: The Race to Protect Legacy Rates

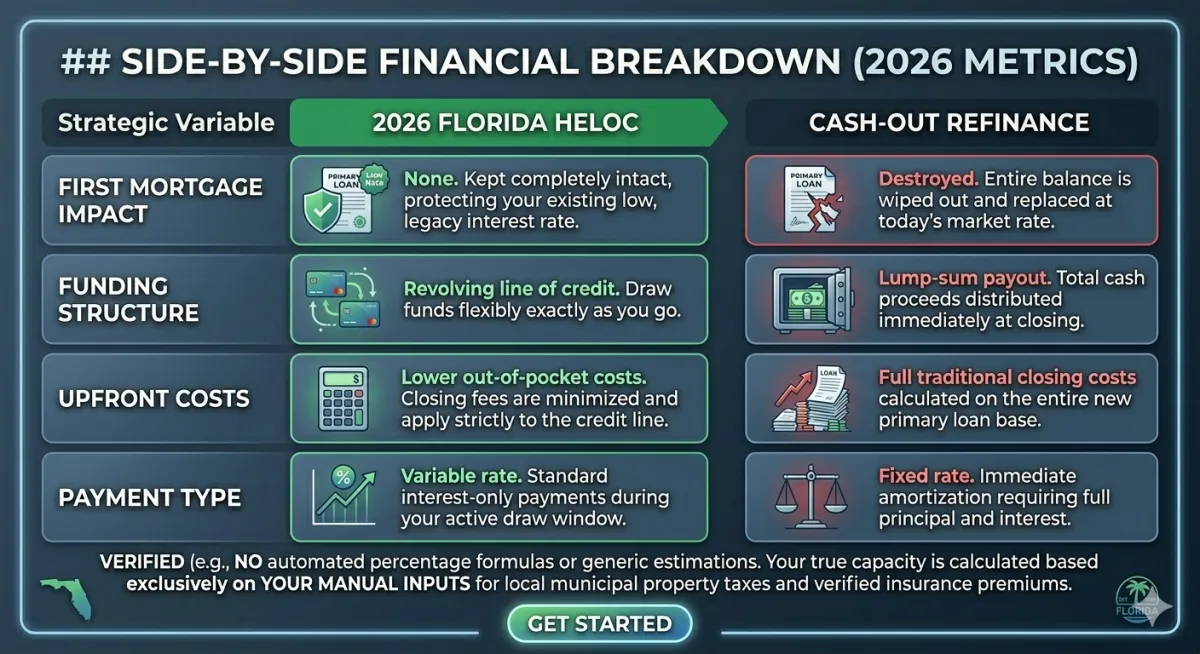

The defining mortgage trend of 2026 is the battle over the first lien. A massive percentage of Florida homeowners are holding historic primary mortgage rates locked in at 3% to 4% from a few years ago.

The Cash-Out Refinance Stumble: A cash-out refinance requires you to completely wipe out your existing first mortgage and replace it with a brand-new, larger loan at current market rates, which are hovering around 6.5% to 7%. Forcing a low 3.5% rate up to 6.85% across your entire housing debt is an expensive way to get cash.

The HELOC Surge: Because of this "rate lock-in" effect, HELOC balances are climbing steadily across the country. A HELOC acts as a standalone second mortgage. It leaves your low-rate first mortgage entirely untouched while giving you a separate, flexible line of credit (typically averaging around 7% APR this year) strictly for the cash you need.

### How Florida Property Values Control Your Borrowing Power Today

Your actual borrowing power is dictated by your Combined Loan-to-Value (CLTV) ratio—the relationship between your total mortgage debt and your home's current appraised value. This is where the localized 2026 Florida market comes into play.

The era of double-digit annual appreciation has leveled off into a phase of healthy stabilization. Statewide, the median single-family home price has settled tightly between $417,000 and $420,000. However, Florida is currently a "split market," meaning your geographic location drastically alters your equity pool:

Growth Hubs (Expanding Equity): Metros like Tampa-St. Petersburg-Clearwater continue to show resilient upward movement, tracking a +2.5% year-over-year increase in median prices (averaging around $405,000 to $450,000). If you own property here, your borrowing power is actively expanding.

Softening Zones (Capped Equity): Other areas, such as Panama City (-5.8%) or Cape Coral-Fort Myers (-2.4%), are experiencing modest price softening as active inventory climbs. In these regions, your borrowing power is flat or slightly compressed, meaning appraisal precision is everything.

The Math: Standard 85% CLTV Cap

Most equity programs limit your total exposure to 85% CLTV. If a stabilizing market anchors your home value at $450,000, your absolute maximum combined loan threshold is $382,500 ($450,000 \times 0.85$). If your primary mortgage balance is $250,000, your maximum equity withdrawal via a HELOC is capped at exactly $132,500.

### Why Bypassing Automated "Guesstimates" Matters

Many national lending platforms use standardized software scripts that apply flat percentage rules to guess your local real estate costs. They look at your home value and apply automatic assumptions for property taxes and homeowners insurance premiums to calculate your debt-to-income (DTI) ratio.

In Florida, this automated approach completely breaks down. Thanks to local variables like the Save Our Homes tax assessment cap and wildly divergent home insurance premiums based on structural wind mitigation features, your true bills cannot be guessed by an algorithm. If a generic calculator overestimates your insurance premium, it artificially inflates your DTI and slashes your approved credit limit.

That is why FloridaHELOCLine.com is built entirely on manual user data entry. We throw out the algorithmic guesswork. You input your exact, verified county tax bill and true annual insurance premium, allowing our 23-year broker network to maximize your actual borrowing power with flawless accuracy.

### The Strategic Summary

If your primary mortgage rate is under 5%, current 2026 trends heavily favor a HELOC over a cash-out refinance. It provides the surgical flexibility to leverage your stable Florida property value without resetting your entire financial foundation.