Maximize Your Borrowing Power with a First Lien HELOC

First Lien HELOC

Are you looking for a smarter way to leverage your home equity without the rigidity of a traditional mortgage? Our First Lien Home Equity Line of Credit (HELOC) combines your primary mortgage and a revolving line of credit into one powerful financial tool.

Why Choose a First Position HELOC?

Unlike a standard second mortgage, a First Position HELOC replaces your existing mortgage entirely. This allows you front-of-the-line access to your home's value with simplified monthly payments and enhanced liquidity.

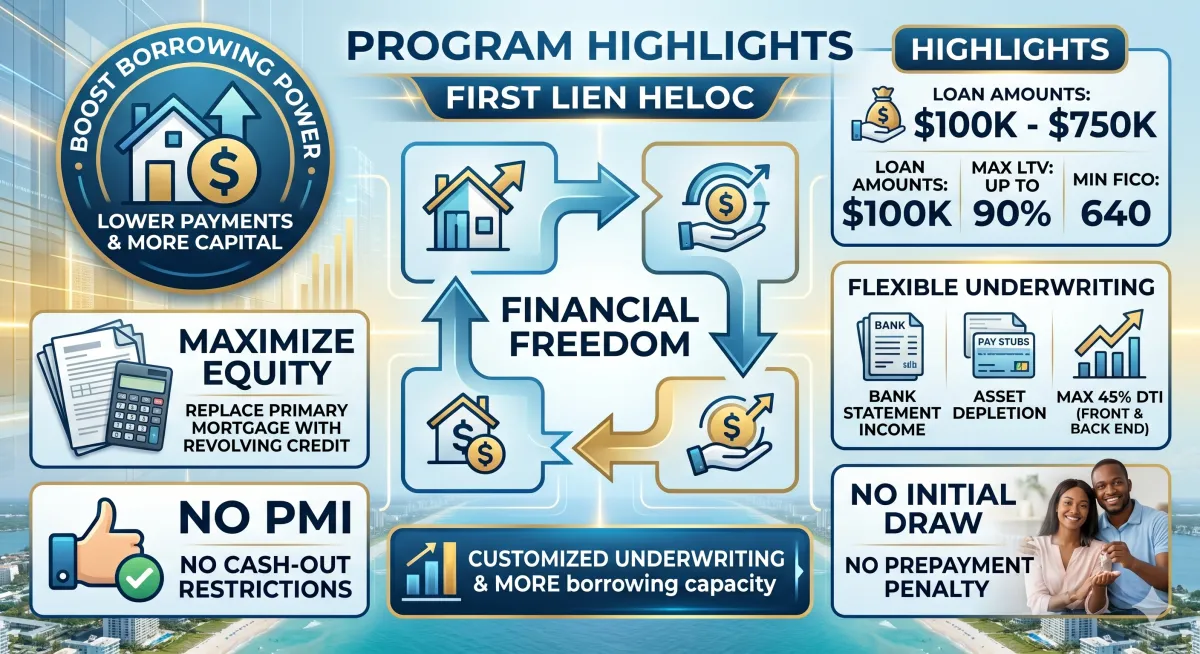

Key Program Highlights:

For properties with no current mortgage Free And Clear

High Leverage: Access up to 90% Loan-to-Value (LTV) to maximize your available cash.

Flexible Income Qualification: We offer Bank Statement Income and Asset Depletion programs, perfect for self-employed borrowers or retirees.

Lower Entry Barriers: Qualify with a 640 minimum FICO score.

Debt Consolidation: Combine high-interest debt and multiple mortgages into one interest-only payment during the draw period.

No Monthly "Hidden" Costs: Enjoy No Private Mortgage Insurance (PMI) and No Prepayment Penalties.

HELOC Estimator

Assumes full line utilization at the stated interest rate.

Frequently Asked Questions

What is the difference between a first and second lien HELOC?

The main difference is priority position. A first lien HELOC replaces your original mortgage, becoming the primary debt on the property. A second lien HELOC sits "behind" your existing mortgage and often carries higher interest rates.

Can I use bank statements to qualify for a HELOC?

Yes. Our customized underwriting allows for Bank Statement Income. This is an ideal solution for business owners or those with unconventional income who may not have traditional tax returns. The Max LTV is 65%.

Is a First Lien HELOC better than a cash-out refinance?

It depends on your need for flexibility. A cash-out refinance provides a lump sum with a fixed payment, whereas a HELOC is a revolving line. You only pay interest on what you actually draw, making it a more efficient tool for ongoing projects or emergency funds.